If you own a home in the Greater New Orleans area or on the Northshore, there is a number attached to your property that affects your mortgage, your insurance premium, and your financial exposure to one of the most common disasters in Louisiana. That number — or more accurately, that letter — is your FEMA flood zone designation.

And yet, most Louisiana homeowners have no idea what their flood zone actually means, how it was determined, or why it matters so much. At Chabert Insurance The Ehrhardt Agency, we talk about flood zones with clients every single day. So let’s clear it up once and for all.

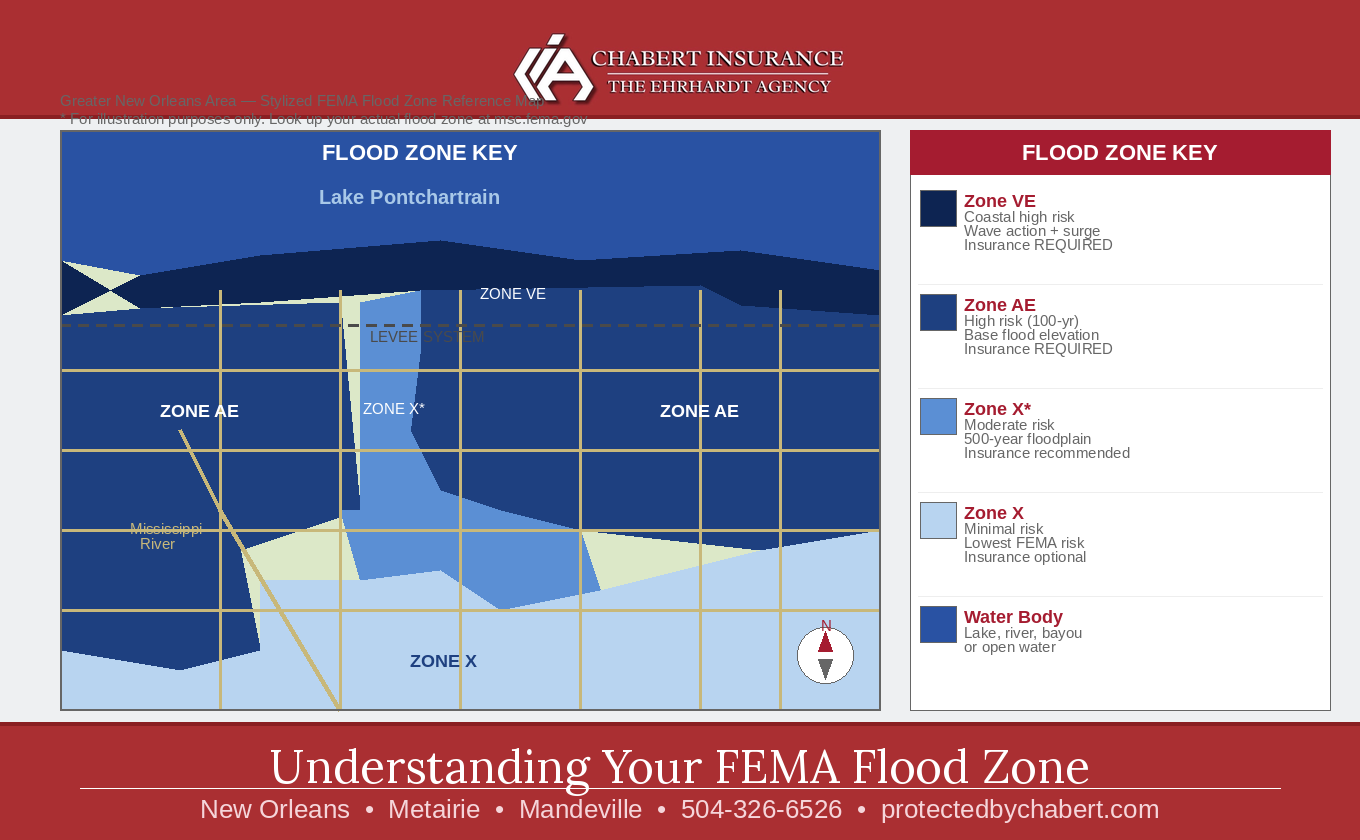

What Is a FEMA Flood Map?

FEMA’s Flood Insurance Rate Maps — known as FIRMs — are the official government maps that show the flood risk for every piece of land in the country. These maps are created using detailed engineering studies, historical flood data, elevation surveys, storm modeling, and drainage analysis.

The maps divide land into flood zones based on the statistical probability of flooding in any given year. Your flood zone designation tells lenders, insurers, and local governments how likely your property is to flood — and at what level.

In Southeast Louisiana, FEMA flood maps cover Orleans Parish, Jefferson Parish, St. Tammany Parish, St. Charles Parish, St. Bernard Parish, and the surrounding areas. The maps are updated periodically as new data becomes available, new levees are built, and development patterns change across the region.

You can look up your property’s official flood zone designation at FEMA’s Flood Map Service Center at msc.fema.gov — just enter your address and your Flood Insurance Rate Map will pull up.

Breaking Down the Flood Zone Designations

Here is what each flood zone designation actually means for homeowners in the New Orleans metro area and Northshore:

| Zone | What It Means | Flood Insurance Required? |

| Zone AE | High-risk zone. Has a 1% annual chance of flooding (the ‘100-year flood’). Base Flood Elevations are established. | Yes — required for federally backed mortgages |

| Zone A | High-risk zone. 1% annual chance of flooding but no Base Flood Elevation established. | Yes — required for federally backed mortgages |

| Zone VE / V | Coastal high-risk zone subject to wave action in addition to flooding. Most severe designation. | Yes — required for federally backed mortgages |

| Zone X (Shaded) | Moderate risk. 0.2% annual chance of flooding (the ‘500-year flood’). Between the 100-year and 500-year floodplain. | Not required — but strongly recommended |

| Zone X (Unshaded) | Minimal risk area. Outside the 500-year floodplain. Considered low risk. | Not required — but still possible to flood |

The ‘100-Year Flood’ — The Most Misunderstood Term in Insurance

When you hear that a property is in the ‘100-year floodplain,’ most people assume it means the area only floods once every hundred years. That is one of the most dangerous misconceptions in the insurance world — and in Louisiana, it can cost you everything.

The 100-year flood designation does not mean a flood happens once a century. It means there is a 1% chance of a flood of that magnitude occurring in any given year. That may sound small, but consider this: over the course of a 30-year mortgage, a home in the 100-year floodplain has roughly a 26% chance of experiencing a flood event.

In Louisiana, where major storms arrive with regularity and drainage infrastructure is constantly tested, the statistical risk is even more meaningful than those numbers suggest. Orleans and Jefferson Parishes have among the highest concentrations of repetitive flood loss properties in the entire country — properties that have flooded not once, not twice, but multiple times.

Being Outside a Flood Zone Does Not Mean You Are Safe

This is perhaps the most important point we make to homeowners across the Northshore and Greater New Orleans area: being outside a high-risk flood zone does not mean your home cannot flood. It simply means FEMA has determined the statistical probability is lower.

The data backs this up clearly. Nationally, roughly 25% of all flood insurance claims are filed by properties located outside of high-risk flood zones. In a state like Louisiana — where heavy rainfall events, overwhelmed drainage systems, and hurricane storm surge routinely affect neighborhoods well outside mapped floodplains — that number is especially relevant.

Think about the flooding that occurred across the Northshore during the August 2016 flood event. Tens of thousands of homes in St. Tammany Parish and surrounding areas flooded — many of them in Zone X, where flood insurance was not required and many homeowners did not have it. The damage was catastrophic precisely because so many people assumed they were safe.

| The Hard Truth Being in Zone X or outside a mapped flood zone is not a guarantee that your home will not flood. It is a statistical designation based on modeling — not a promise. Every home in Southeast Louisiana has some level of flood risk. The only question is whether you are financially prepared if it happens. |

How Flood Zone Designations Affect Your Insurance and Mortgage

Your flood zone designation has direct, real-world financial consequences. Here is how it affects you:

Federally Backed Mortgages

If your home is in a high-risk flood zone (Zone A, AE, V, or VE) and you have a mortgage backed by a federal lender — which includes most conventional mortgages — you are legally required to carry flood insurance. Your lender will verify this at closing and every year thereafter. If you let your flood policy lapse, your lender can force-place coverage on your behalf, which is almost always far more expensive than purchasing it yourself.

Insurance Premiums

Your flood zone designation is one of the primary factors that determines your flood insurance premium. Properties in Zone AE or VE will typically carry higher premiums than those in Zone X. However, since FEMA introduced Risk Rating 2.0 in 2021 and 2022, flood insurance pricing has shifted to reflect each property’s individual risk characteristics — including elevation, distance from water, and foundation type — rather than relying solely on flood zone designation.

This means that some Zone X properties have seen premium increases under the new system, while some Zone AE properties have seen decreases, depending on their specific risk profile.

Home Sales and Purchases

When you buy or sell a home in Louisiana, the flood zone designation plays a significant role. Buyers in high-risk zones must factor the cost of mandatory flood insurance into their monthly housing budget. Sellers in high-risk zones are required to disclose the property’s flood zone status. And when a property is remapped from a lower-risk zone to a higher-risk zone, it can affect the home’s marketability and value.

What Are FEMA Map Updates — and Why Should You Pay Attention?

FEMA periodically revises flood maps to account for new data, infrastructure changes, and updated storm modeling. In recent years, Southeast Louisiana has seen significant map revisions affecting Orleans, Jefferson, St. Tammany, and St. Charles Parishes — with expanded AE zones in some areas and revised V zones near Lake Pontchartrain reflecting updated wave and surge modeling.

When a map update places your property in a higher-risk zone, it can trigger mandatory flood insurance requirements and affect your premium. When a map update moves your property to a lower-risk zone, you may have the opportunity to reduce your premium or adjust your coverage.

The key takeaway: your flood zone designation today may not be your flood zone designation in five years. Staying informed about map updates in your parish is an important part of managing your risk and your insurance costs as a Louisiana homeowner.

NFIP vs. Private Flood Insurance — Which Is Right for You?

Most flood insurance in Louisiana is purchased through the National Flood Insurance Program — the federal government-backed program administered by FEMA. NFIP policies are available to homeowners, renters, and business owners in participating communities and offer up to $250,000 in building coverage and $100,000 in contents coverage.

However, private flood insurance has grown significantly in recent years and offers some important advantages worth discussing with your agent:

- Higher coverage limits — private policies can often exceed the NFIP’s $250,000 building cap, which is important for higher-value homes.

- Additional coverages — some private policies include loss of use coverage and other features not available through the NFIP.

- Competitive pricing — for lower-risk properties, private flood insurance can sometimes be less expensive than an NFIP policy under Risk Rating 2.0.

- Shorter waiting periods — some private carriers offer shorter waiting periods than the NFIP’s standard 30 days.

As an independent insurance agency, Chabert Insurance The Ehrhardt Agency can help you compare both NFIP and private flood insurance options to find the right fit for your home and budget.

How to Look Up Your Flood Zone — and What to Do Next

Looking up your flood zone is simple. Here is how:

- Go to msc.fema.gov — FEMA’s Flood Map Service Center.

- Enter your property address in the search bar.

- Your Flood Insurance Rate Map will appear, showing your zone designation.

- You can also contact your parish floodplain administrator, or simply call us and we can help walk you through what it means.

Once you know your zone, the next step is making sure your coverage is appropriate. If you are in a high-risk zone, your flood coverage limits should reflect the actual cost to rebuild your home — not just meet the mortgage lender’s minimum requirement. If you are in Zone X, we strongly encourage you to consider a flood policy anyway, given Louisiana’s track record with flooding events that go well beyond what any map can predict.

| Not Sure What Your Flood Zone Means for Your Coverage? We help homeowners across New Orleans, Metairie, Mandeville, Covington, and the entire Southeast Louisiana area understand their flood risk and make sure their coverage is right. Let’s talk before the next storm season. 📞 Call or Text: 504-326-6526 🌐 Visit: protectedbychabert.com 📍 Mandeville & New Orleans, Louisiana |