A multi-vehicle accident can become complicated fast. When several drivers are involved, insurance carriers may need time to review statements, vehicle damage, and the order of impact before determining who is responsible. In Louisiana, fault plays a central role in how an auto insurance claim moves forward, which can make these crashes more stressful for drivers trying to recover and get back on the road.

For drivers in Mandeville, LA, this means a claim may not move as smoothly as it would after a simple two-car collision. Chabert Insurance of the Northshore helps local drivers understand that when fault is disputed, compensation can take longer, especially if multiple insurers are involved. That is one reason a strong auto insurance review matters before an accident ever happens.

What Can Slow Down an Auto Insurance Claim?

In a multi-vehicle collision, each insurance company may evaluate the accident differently. One carrier may see one driver as primarily responsible, while another may continue investigating. This can affect how quickly property damage claims, vehicle repair questions, and injury-related concerns are addressed.

Common Issues Drivers May Face After a Multi-Car Wreck

Conflicting accounts from multiple drivers and witnesses

Delays while insurers review liability and claim details

Questions about which coverage responds first

Added stress when damage and injuries involve several vehicles

Why Coverage Reviews Matter Before an Accident Happens

Because Louisiana follows a fault-based system, drivers should understand their liability protection, medical-related coverages, and optional policy features before they need them. Chabert Insurance of the Northshore works with drivers who want a clearer picture of how their policy may respond after a serious crash.

Buying your first home is one of the most exciting milestones of your life. It is also one of the most overwhelming — and in Louisiana, that process comes with a layer of complexity that first-time buyers in other states simply do not face. Between a challenging insurance market, mandatory flood coverage requirements, hurricane season, and a carrier landscape unlike anywhere else in the country, navigating home insurance as a new Louisiana homeowner can feel like learning a foreign language overnight.

At Chabert Insurance The Ehrhardt Agency, we work with first-time homebuyers across the Greater New Orleans area and the Northshore every single week. We know the questions you are asking, the surprises that catch buyers off guard, and the mistakes that are easy to avoid if you know what to look for. This guide is designed to walk you through everything you need to know — before you close, before you sign, and before you make a decision you will regret.

Why Home Insurance in Louisiana Is Different

Let’s start with the honest truth: homeowners insurance in Louisiana is more expensive, more complicated, and harder to get than in most other states. The average cost of homeowners insurance in Louisiana is approximately $2,835 per year — about 32% higher than the national average. For many first-time buyers, this comes as a significant shock, especially when the insurance cost is not factored into their original budget.

The reasons behind these higher costs are deeply rooted in Louisiana’s geography and history. The state sits in the direct path of Gulf Coast hurricanes, its coastal land is disappearing at one of the fastest rates in the world, much of the Greater New Orleans area sits below sea level, and the state has experienced more catastrophic flood losses than almost anywhere else in the country. Since hurricanes Katrina and Ida, dozens of national insurance carriers have reduced their presence in Louisiana or exited the market entirely, leaving fewer options and higher prices for homeowners.

Understanding this context before you start shopping for a home will help you budget accurately, ask better questions, and make smarter decisions throughout the homebuying process.

When Do You Need Home Insurance — and Why Your Lender Requires It?

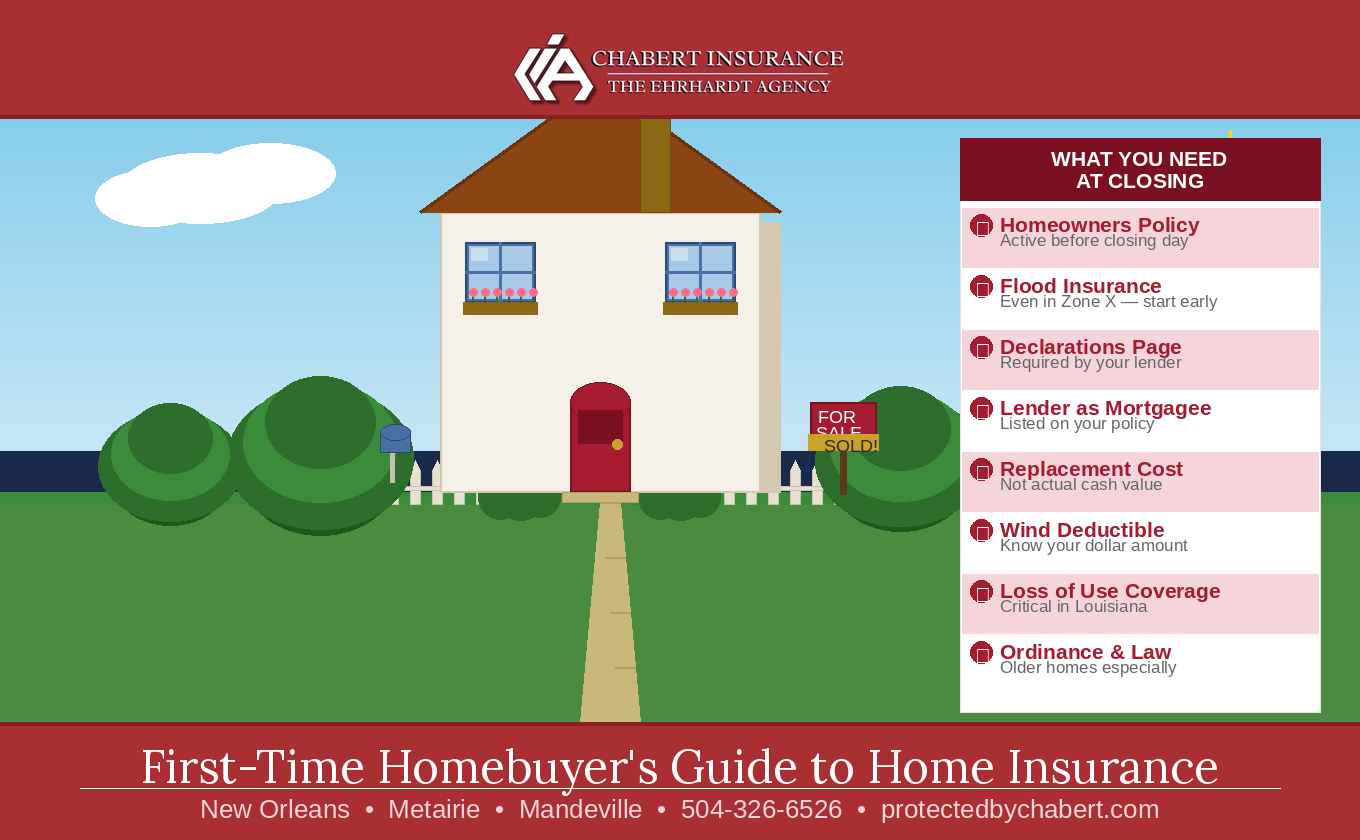

If you are financing your home purchase with a mortgage — which most first-time buyers do — your lender will require you to have an active homeowners insurance policy in place before you can close. This is not optional. Without proof of insurance, your closing will not happen.

The reason lenders require this is straightforward: your home is the collateral for your loan. If your home burns down or is destroyed by a hurricane, the lender wants to know that the asset securing their investment is protected. The insurance policy protects both you and the bank.

Most lenders will require you to provide a declarations page — a one-page summary of your policy details — before closing. Your lender will also typically require that they be listed on the policy as an Additional Insured or Mortgagee, meaning they receive notice if your policy lapses or is cancelled. This is standard practice and nothing to be alarmed by.

Start Early Do not wait until the week before closing to start shopping for home insurance. In Louisiana’s complicated market, getting quotes, comparing options, and binding a policy can take longer than you expect. We recommend starting the insurance conversation at least 30-45 days before your expected closing date — ideally as soon as your offer is accepted.

Understanding What a Homeowners Policy Actually Covers

A standard homeowners insurance policy is made up of several coverage components. Understanding each one — and how it applies specifically to Louisiana — is essential for making sure your policy is truly protecting you.

Coverage Type

What It Covers

Louisiana Importance

Dwelling (Coverage A)

The structure of your home — walls, roof, floors, built-in appliances.

Critical — rebuild costs in Louisiana are high due to storm damage demand.

Other Structures (Coverage B)

Detached garage, fence, shed, carport.

Often overlooked but important for Louisiana properties.

Personal Property (Coverage C)

Furniture, electronics, clothing, and belongings inside the home.

Make sure limits are adequate — contents claims are very common after storms.

Loss of Use (Coverage D)

Pays for hotel, meals, and living expenses if your home is uninhabitable.

Essential in Louisiana — hurricane and flood damage can displace families for months.

Liability (Coverage E)

Protects you if someone is injured on your property.

Important for pools, trampolines, and high-traffic properties.

Medical Payments (Coverage F)

Pays medical bills for guests injured on your property regardless of fault.

Provides a layer of protection before liability claims escalate.

The Louisiana-Specific Coverages Every First-Time Buyer Needs to Understand

Beyond the standard components of a homeowners policy, there are several Louisiana-specific coverage issues that every first-time buyer needs to understand before purchasing a home in our market.

1. Flood Insurance — The Most Critical Conversation

Your homeowners policy does not cover flood damage. This is one of the most important things to understand as a first-time buyer in Louisiana. Flood insurance is an entirely separate policy that must be purchased independently — either through the National Flood Insurance Program (NFIP) or through a private flood carrier.

If your home is in a high-risk flood zone (Zone A, AE, V, or VE) and you have a federally backed mortgage, flood insurance is legally required. But even if your home is in a lower-risk Zone X designation, we strongly recommend purchasing flood coverage. Nationally, about 25% of all flood insurance claims come from properties outside of high-risk zones — and in a state like Louisiana, that risk is even more real.

There is also a critical timing issue: NFIP flood policies have a standard 30-day waiting period before they go into effect. If you wait until a storm is approaching or named, it is too late. Get your flood policy in place at closing — or ideally, before.

2. Wind and Hail Deductibles — Know Your Number Before You Close

In Louisiana, most homeowners policies include a separate, higher deductible that applies specifically to wind and hail damage — the type of damage most commonly associated with hurricanes. This deductible is typically expressed as a percentage of your home’s insured value rather than a flat dollar amount.

On a $300,000 home, a 2% wind deductible means you would pay $6,000 out of pocket before insurance kicks in for wind damage. A 5% deductible means $15,000. As a first-time buyer, make sure you know exactly what your wind deductible is before you bind the policy — and make sure you have sufficient savings to cover it if a storm hits.

3. Replacement Cost vs. Actual Cash Value

When your home or belongings are damaged, how your policy pays out makes an enormous difference. There are two primary methods:

Replacement Cost Value (RCV) — Pays what it actually costs to repair or replace the damaged item at today’s prices. This is the coverage you want.

Actual Cash Value (ACV) — Pays the depreciated value of the item, accounting for age and wear. On a 15-year-old roof, this could pay out a fraction of what a new roof actually costs.

In Louisiana, where construction costs have risen significantly since recent storms, the gap between ACV and RCV payouts can be staggering. Always confirm that your dwelling coverage is written on a Replacement Cost basis — and ask specifically whether your personal property coverage is RCV or ACV as well.

4. Ordinance or Law Coverage

Louisiana has significant building code requirements that have been updated substantially since older homes were constructed. If your home is damaged and local codes require you to bring the entire structure up to current standards during the repair — not just fix the damaged portion — Ordinance or Law coverage pays for that additional cost. Without it, you could face tens of thousands of dollars in unexpected expenses that your standard policy will not cover. This is especially important for buyers purchasing older homes in New Orleans, Metairie, and other historic neighborhoods.

5. Loss of Use Coverage — More Important Than You Think

If your home becomes uninhabitable after a covered event — whether it is a hurricane, fire, or major water damage — Loss of Use coverage pays for your temporary living expenses. This includes hotel stays, restaurant meals, and other costs above what you normally spend. In Louisiana, where major storm damage can displace families for months or even years, having adequate Loss of Use limits is not a luxury — it is a necessity. Review your policy’s Loss of Use limits carefully and make sure they reflect the realistic cost of alternative housing in your area.

How Much Home Insurance Do You Actually Need?

One of the most common mistakes first-time buyers make is insuring their home for the purchase price rather than the rebuild cost. These are two very different numbers.

The purchase price of a home includes the value of the land — which cannot be destroyed in a storm. What your insurance needs to cover is the cost to completely rebuild the structure from the ground up if it were totally destroyed. In Louisiana, rebuild costs have increased significantly due to material and labor costs driven by post-storm demand across the Gulf Coast.

Your insurance agent can help you run a replacement cost estimator to determine the appropriate dwelling coverage amount for your specific home. Do not simply accept the minimum coverage your lender requires — that number is based on the outstanding loan balance, not the actual cost to rebuild your home. Make sure the two align or that you are fully aware of the gap.

The Louisiana Insurance Market — What First-Time Buyers Need to Know

Louisiana’s homeowners insurance market is unlike any other in the country. Since hurricanes Katrina, Gustav, Ike, Laura, Delta, Zeta, and Ida, the carrier landscape has been fundamentally reshaped. Many national carriers have significantly reduced their appetite for new Louisiana business, exited the state entirely, or non-renewed large portions of their books.

This means that as a first-time buyer, you may find that your options are more limited — and more expensive — than you expected. It also means that working with an independent insurance agent who knows the Louisiana market is more valuable than ever. Unlike a captive agent who can only offer products from one carrier, an independent agent like Chabert Insurance The Ehrhardt Agency shops across multiple carriers — including admitted carriers, surplus lines markets, and specialty programs — to find the best available option for your specific home.

There are also things you can do before you purchase a home to improve your insurability and reduce your costs:

Ask about the home’s claims history — a property with multiple prior claims may be difficult or expensive to insure.

Check the condition of the roof — most carriers will not write a policy on a roof over 20 years old, and some have stricter cutoffs.

Ask about the home’s elevation certificate if it is in or near a flood zone — this document can significantly affect your flood insurance premium.

Look into the Fortified Home program — a Louisiana-specific construction standard that can qualify your home for premium discounts.

First-Time Homebuyer Programs in Louisiana — Don’t Overlook These

Louisiana has several programs specifically designed to help first-time buyers — and some of them can help offset your insurance and closing costs. Here are the most important ones to know about:

Louisiana Housing Corporation (LHC) Programs

The LHC offers several mortgage programs for first-time buyers, including the MRB Home program for buyers earning 80% or less of the area median income, which offers below-market interest rates and between 5-9% of the mortgage amount in down payment and closing cost assistance. The MRB Assisted program serves buyers in targeted areas earning up to 140% of AMI.

New Orleans Direct Homebuyer Assistance Program

The City of New Orleans offers eligible first-time buyers up to $55,000 as a forgivable soft second mortgage for down payment assistance, plus $5,000 in closing cost assistance. The program is income-limited (80% of AMI for the area) and the home must be priced at $324,000 or below. The assistance is forgivable after 10 years.

Jefferson Parish First-Time Homebuyer Assistance

Jefferson Parish offers eligible first-time buyers up to $50,000 (or $60,000 in Kenner) as a forgivable loan for down payment and closing cost assistance. Like the New Orleans program, income limits and purchase price caps apply.

These programs can make a meaningful difference in your ability to afford both your down payment and your first year of insurance premiums. Ask your lender and your insurance agent about all available options early in the process.

Your Home Insurance Checklist Before Closing

Here is a simple checklist every first-time buyer in Louisiana should work through before closing day:

Start shopping for homeowners insurance at least 30-45 days before your expected closing date.

Work with an independent agent who can compare multiple carriers — not just one company.

Confirm your dwelling coverage is based on replacement cost, not purchase price.

Ask specifically about your wind and hail deductible — and make sure you understand the dollar amount.

Purchase a flood insurance policy at closing — even if you are not in a high-risk zone.

Ask about Ordinance or Law coverage, especially if buying an older home.

Review your Loss of Use coverage limits — make sure they are adequate for Louisiana housing costs.

Get a copy of the home’s prior claims history (your agent can help with this).

Ask about the roof age and condition before closing — this affects your coverage options and premium.

If the home is in or near a flood zone, ask for an elevation certificate.

Confirm your lender is listed as the Mortgagee on your homeowners policy before closing.

Keep a copy of your declarations page in a safe place — digital and physical.

A Note from Chabert Insurance We know the Louisiana insurance market is frustrating — especially for first-time buyers who are already managing so many moving parts. Our job is to take that burden off your plate. We will shop your coverage, explain your options in plain language, make sure your policy meets your lender’s requirements, and make sure you are genuinely protected — not just checking a box. Call or text us at 504-326-6526. We are here to help.

Buying Your First Home in Louisiana? Let Chabert Insurance The Ehrhardt Agency walk you through your options and make sure you are properly protected from day one. We serve first-time buyers across New Orleans, Metairie, Mandeville, Covington, Slidell, and all of Southeast Louisiana. 📞 Call or Text: 504-326-6526🌐 Visit: protectedbychabert.com 📍 Mandeville & New Orleans, Louisiana

If you own a home in the Greater New Orleans area or on the Northshore, there is a number attached to your property that affects your mortgage, your insurance premium, and your financial exposure to one of the most common disasters in Louisiana. That number — or more accurately, that letter — is your FEMA flood zone designation.

And yet, most Louisiana homeowners have no idea what their flood zone actually means, how it was determined, or why it matters so much. At Chabert Insurance The Ehrhardt Agency, we talk about flood zones with clients every single day. So let’s clear it up once and for all.

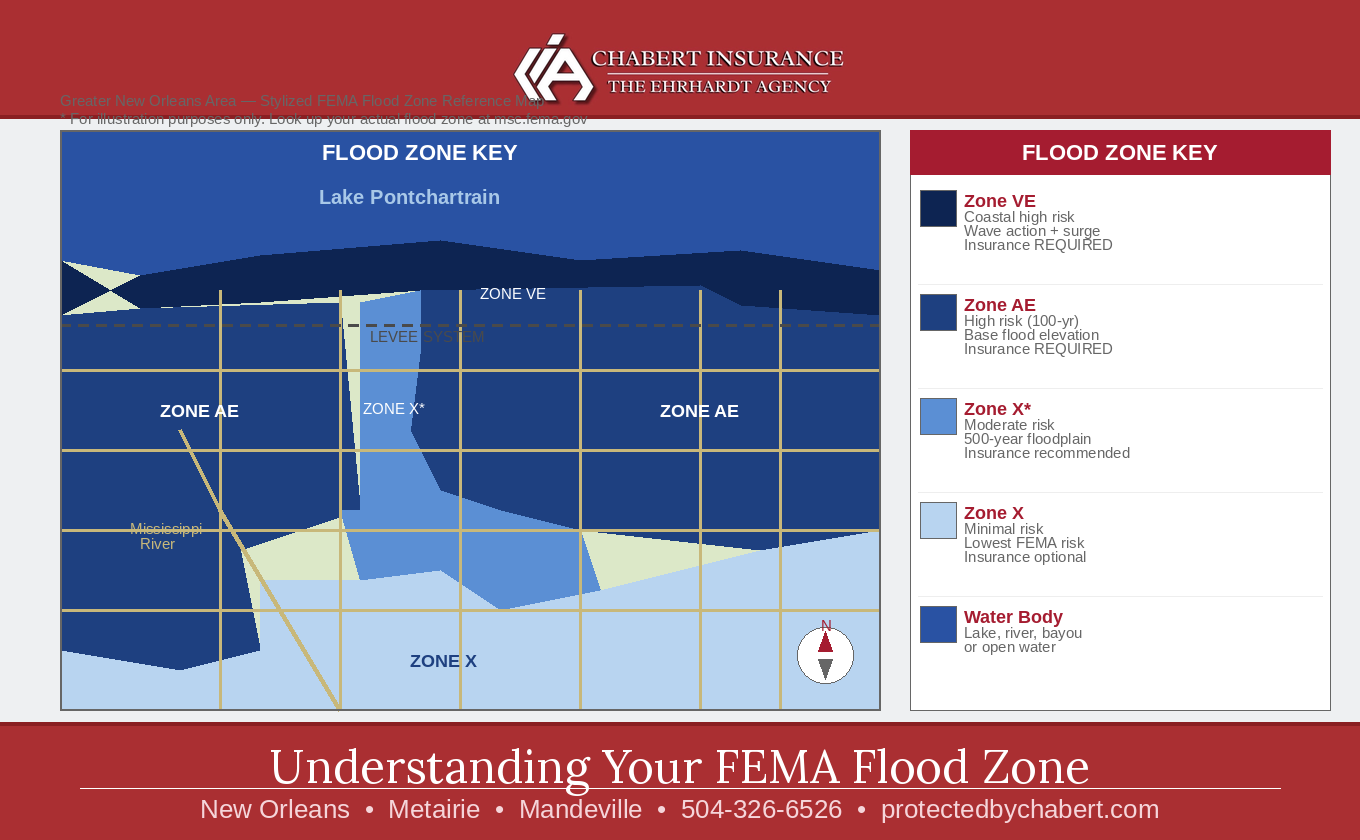

What Is a FEMA Flood Map?

FEMA’s Flood Insurance Rate Maps — known as FIRMs — are the official government maps that show the flood risk for every piece of land in the country. These maps are created using detailed engineering studies, historical flood data, elevation surveys, storm modeling, and drainage analysis.

The maps divide land into flood zones based on the statistical probability of flooding in any given year. Your flood zone designation tells lenders, insurers, and local governments how likely your property is to flood — and at what level.

In Southeast Louisiana, FEMA flood maps cover Orleans Parish, Jefferson Parish, St. Tammany Parish, St. Charles Parish, St. Bernard Parish, and the surrounding areas. The maps are updated periodically as new data becomes available, new levees are built, and development patterns change across the region.

You can look up your property’s official flood zone designation at FEMA’s Flood Map Service Center at msc.fema.gov — just enter your address and your Flood Insurance Rate Map will pull up.

Breaking Down the Flood Zone Designations

Here is what each flood zone designation actually means for homeowners in the New Orleans metro area and Northshore:

Zone

What It Means

Flood Insurance Required?

Zone AE

High-risk zone. Has a 1% annual chance of flooding (the ‘100-year flood’). Base Flood Elevations are established.

Yes — required for federally backed mortgages

Zone A

High-risk zone. 1% annual chance of flooding but no Base Flood Elevation established.

Yes — required for federally backed mortgages

Zone VE / V

Coastal high-risk zone subject to wave action in addition to flooding. Most severe designation.

Yes — required for federally backed mortgages

Zone X (Shaded)

Moderate risk. 0.2% annual chance of flooding (the ‘500-year flood’). Between the 100-year and 500-year floodplain.

Not required — but strongly recommended

Zone X (Unshaded)

Minimal risk area. Outside the 500-year floodplain. Considered low risk.

Not required — but still possible to flood

The ‘100-Year Flood’ — The Most Misunderstood Term in Insurance

When you hear that a property is in the ‘100-year floodplain,’ most people assume it means the area only floods once every hundred years. That is one of the most dangerous misconceptions in the insurance world — and in Louisiana, it can cost you everything.

The 100-year flood designation does not mean a flood happens once a century. It means there is a 1% chance of a flood of that magnitude occurring in any given year. That may sound small, but consider this: over the course of a 30-year mortgage, a home in the 100-year floodplain has roughly a 26% chance of experiencing a flood event.

In Louisiana, where major storms arrive with regularity and drainage infrastructure is constantly tested, the statistical risk is even more meaningful than those numbers suggest. Orleans and Jefferson Parishes have among the highest concentrations of repetitive flood loss properties in the entire country — properties that have flooded not once, not twice, but multiple times.

Being Outside a Flood Zone Does Not Mean You Are Safe

This is perhaps the most important point we make to homeowners across the Northshore and Greater New Orleans area: being outside a high-risk flood zone does not mean your home cannot flood. It simply means FEMA has determined the statistical probability is lower.

The data backs this up clearly. Nationally, roughly 25% of all flood insurance claims are filed by properties located outside of high-risk flood zones. In a state like Louisiana — where heavy rainfall events, overwhelmed drainage systems, and hurricane storm surge routinely affect neighborhoods well outside mapped floodplains — that number is especially relevant.

Think about the flooding that occurred across the Northshore during the August 2016 flood event. Tens of thousands of homes in St. Tammany Parish and surrounding areas flooded — many of them in Zone X, where flood insurance was not required and many homeowners did not have it. The damage was catastrophic precisely because so many people assumed they were safe.

The Hard Truth Being in Zone X or outside a mapped flood zone is not a guarantee that your home will not flood. It is a statistical designation based on modeling — not a promise. Every home in Southeast Louisiana has some level of flood risk. The only question is whether you are financially prepared if it happens.

How Flood Zone Designations Affect Your Insurance and Mortgage

Your flood zone designation has direct, real-world financial consequences. Here is how it affects you:

Federally Backed Mortgages

If your home is in a high-risk flood zone (Zone A, AE, V, or VE) and you have a mortgage backed by a federal lender — which includes most conventional mortgages — you are legally required to carry flood insurance. Your lender will verify this at closing and every year thereafter. If you let your flood policy lapse, your lender can force-place coverage on your behalf, which is almost always far more expensive than purchasing it yourself.

Insurance Premiums

Your flood zone designation is one of the primary factors that determines your flood insurance premium. Properties in Zone AE or VE will typically carry higher premiums than those in Zone X. However, since FEMA introduced Risk Rating 2.0 in 2021 and 2022, flood insurance pricing has shifted to reflect each property’s individual risk characteristics — including elevation, distance from water, and foundation type — rather than relying solely on flood zone designation.

This means that some Zone X properties have seen premium increases under the new system, while some Zone AE properties have seen decreases, depending on their specific risk profile.

Home Sales and Purchases

When you buy or sell a home in Louisiana, the flood zone designation plays a significant role. Buyers in high-risk zones must factor the cost of mandatory flood insurance into their monthly housing budget. Sellers in high-risk zones are required to disclose the property’s flood zone status. And when a property is remapped from a lower-risk zone to a higher-risk zone, it can affect the home’s marketability and value.

What Are FEMA Map Updates — and Why Should You Pay Attention?

FEMA periodically revises flood maps to account for new data, infrastructure changes, and updated storm modeling. In recent years, Southeast Louisiana has seen significant map revisions affecting Orleans, Jefferson, St. Tammany, and St. Charles Parishes — with expanded AE zones in some areas and revised V zones near Lake Pontchartrain reflecting updated wave and surge modeling.

When a map update places your property in a higher-risk zone, it can trigger mandatory flood insurance requirements and affect your premium. When a map update moves your property to a lower-risk zone, you may have the opportunity to reduce your premium or adjust your coverage.

The key takeaway: your flood zone designation today may not be your flood zone designation in five years. Staying informed about map updates in your parish is an important part of managing your risk and your insurance costs as a Louisiana homeowner.

NFIP vs. Private Flood Insurance — Which Is Right for You?

Most flood insurance in Louisiana is purchased through the National Flood Insurance Program — the federal government-backed program administered by FEMA. NFIP policies are available to homeowners, renters, and business owners in participating communities and offer up to $250,000 in building coverage and $100,000 in contents coverage.

However, private flood insurance has grown significantly in recent years and offers some important advantages worth discussing with your agent:

Higher coverage limits — private policies can often exceed the NFIP’s $250,000 building cap, which is important for higher-value homes.

Additional coverages — some private policies include loss of use coverage and other features not available through the NFIP.

Competitive pricing — for lower-risk properties, private flood insurance can sometimes be less expensive than an NFIP policy under Risk Rating 2.0.

Shorter waiting periods — some private carriers offer shorter waiting periods than the NFIP’s standard 30 days.

As an independent insurance agency, Chabert Insurance The Ehrhardt Agency can help you compare both NFIP and private flood insurance options to find the right fit for your home and budget.

How to Look Up Your Flood Zone — and What to Do Next

Looking up your flood zone is simple. Here is how:

Go to msc.fema.gov — FEMA’s Flood Map Service Center.

Enter your property address in the search bar.

Your Flood Insurance Rate Map will appear, showing your zone designation.

You can also contact your parish floodplain administrator, or simply call us and we can help walk you through what it means.

Once you know your zone, the next step is making sure your coverage is appropriate. If you are in a high-risk zone, your flood coverage limits should reflect the actual cost to rebuild your home — not just meet the mortgage lender’s minimum requirement. If you are in Zone X, we strongly encourage you to consider a flood policy anyway, given Louisiana’s track record with flooding events that go well beyond what any map can predict.

Not Sure What Your Flood Zone Means for Your Coverage? We help homeowners across New Orleans, Metairie, Mandeville, Covington, and the entire Southeast Louisiana area understand their flood risk and make sure their coverage is right. Let’s talk before the next storm season. 📞 Call or Text: 504-326-6526🌐 Visit: protectedbychabert.com 📍 Mandeville & New Orleans, Louisiana