What Louisiana Homeowners Need to Know About the IBHS FORTIFIED Roof Standard

Louisiana homeowners are paying some of the highest insurance premiums in the country — and for many families across the Greater New Orleans area and the Northshore, the cost of coverage has become as significant a financial burden as the mortgage itself. The average annual homeowners insurance premium in Louisiana now stands at roughly $4,031 — more than $1,600 above the national average — and for coastal and near-coastal properties, that number can climb considerably higher.

Against that backdrop, one program has emerged as one of the most powerful tools available to Louisiana homeowners looking to meaningfully reduce their insurance costs: the FORTIFIED Roof program, administered by the Insurance Institute for Business and Home Safety (IBHS). At Chabert Insurance The Ehrhardt Agency, we talk to clients about FORTIFIED roofs regularly — because for the right home, it can be one of the smartest financial decisions a Louisiana homeowner can make.

This post will walk you through exactly what the FORTIFIED Roof program is, how it works, what the real savings look like, how to get a grant to help cover the cost, and what steps you need to take to put the discount to work on your policy.

What Is the FORTIFIED Roof Program?

FORTIFIED is a voluntary construction standard developed by the Insurance Institute for Business and Home Safety (IBHS) — an independent, nonprofit scientific research organization funded by the insurance industry. The FORTIFIED standard was created to address the specific weaknesses in residential roofing systems that cause the most damage during hurricanes, severe thunderstorms, and high-wind events.

A FORTIFIED roof is not just a new roof. It is a roof built or retrofitted to a significantly higher standard than a typical replacement, using specific techniques and materials designed to dramatically improve wind resistance. The key components that distinguish a FORTIFIED roof from a standard roof include:

- Sealed roof deck — A secondary water barrier is applied to the roof deck so that if shingles are lost in a storm, wind-driven rain cannot enter the home through the exposed decking.

- Enhanced roof attachment — Ring-shank nails driven in a hurricane nailing pattern are used to secure roof decking more firmly to the underlying structure, reducing the risk of deck blow-off.

- Reinforced roof edge — Enhanced edge flashing prevents the peel-back effect that commonly occurs when wind gets under the leading edge of a roof during a storm.

- Impact-rated shingles — High-quality shingles designed to withstand significant hail impact are used, reducing the frequency of weather-related claims.

Once these standards are met and verified by an independent IBHS-certified evaluator, the homeowner receives an official IBHS FORTIFIED Roof certificate — the document that unlocks the insurance discounts and tax benefits that follow.

The Three Levels of FORTIFIED Designation

The FORTIFIED program has three designation levels, each representing a progressively higher standard of resilience. It is important to understand which level qualifies for Louisiana’s insurance discounts:

FORTIFIED Roof (Bronze)

This is the entry-level designation and the one that qualifies for Louisiana’s mandatory insurance discounts under Act 533 (2024). It focuses specifically on the roof — the most vulnerable component of a home in a hurricane — and is the most accessible and affordable starting point for most Louisiana homeowners. This is the designation the Louisiana Fortify Homes Program grant supports.

FORTIFIED Silver

Silver builds on the Roof designation by adding requirements for windows, doors, and attached structures. It provides broader protection against wind damage but is more involved and costly to achieve. Note that Louisiana’s current mandatory discount requirements apply specifically to the FORTIFIED Roof designation — Silver and Gold discounts vary by insurer.

FORTIFIED Gold

The Gold designation is the highest level, adding requirements for the entire structure including walls, foundation connections, and openings. It represents a comprehensively storm-hardened home but is typically pursued for new construction rather than retrofitting an existing home.

How Much Can a FORTIFIED Roof Actually Save You?

This is the question every homeowner asks — and the data from Louisiana is genuinely compelling.

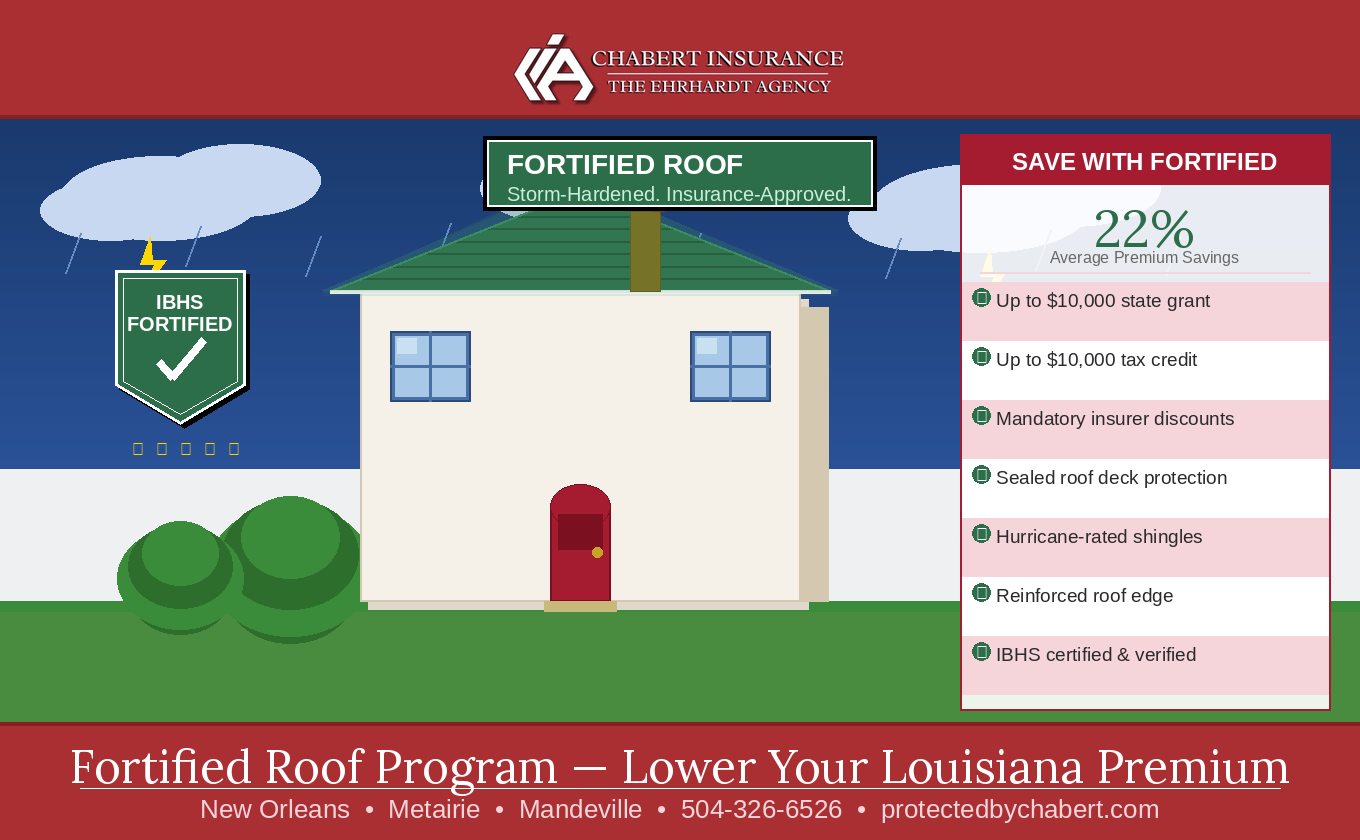

According to a Louisiana Legislative Auditor report, the median homeowner who received a Louisiana Fortify Homes Program grant and installed a FORTIFIED roof saved $1,250 per year on their homeowners insurance — a reduction of approximately 22% in their annual premium. Their median premium dropped from $5,625 to $4,375 annually.

Other data from IBHS and the Louisiana Department of Insurance supports similar findings. Homeowners completing FORTIFIED projects statewide have seen premiums drop an average of 22%, with only about 3.3% of participants experiencing any increase. For many homeowners, the discount is applied primarily to the wind and hail portion of their premium — which is often the largest and fastest-growing component of a Louisiana homeowners policy.

Under Act 533, which took effect in 2024, all admitted insurers in Louisiana are now required by law to offer actuarially justified discounts to homeowners with a valid IBHS FORTIFIED Roof certificate. The Louisiana Department of Insurance issued Bulletin 2025-03 to reinforce this requirement, reminding all insurers and agents of their obligations and confirming that the IBHS FORTIFIED Certificate is the only documentation required to trigger the discount — no additional hurricane loss mitigation forms are needed.

| The Real Numbers Median Louisiana homeowner annual premium: $5,625 Median savings with a FORTIFIED Roof: $1,250 per year (22%) Median post-FORTIFIED annual premium: $4,375 Median FORTIFIED upgrade cost: $16,229 After $10,000 grant (if eligible): $6,229 out of pocket Payback period (after grant): Approximately 5 years Source: Louisiana Legislative Auditor Report |

Louisiana’s FORTIFIED Roof Financial Incentives — A Complete Guide

Louisiana has built one of the most comprehensive support systems in the country for homeowners who want to upgrade to a FORTIFIED roof. Between state grants, federal grants, tax credits, and mandatory insurance discounts, the financial case for upgrading has never been stronger. Here is every incentive currently available:

| Incentive | Amount | Who Qualifies | Notes |

| Louisiana Fortify Homes Program Grant | Up to $10,000 | Owner-occupied primary residence | Awarded via lottery. First-come, first-served grant windows. Must have homestead exemption. |

| FORTIFIED Fund Grant (FHLB) | Up to $15,000 | Income at or below 80% of Area Median Income | Contact FORTIFIEDfund@fhlb.com. Helps lower-income homeowners offset costs. |

| CDBG Grants | Up to $35,000 | Income at or below 80% AMI | Operated with Rebuilding Together New Orleans. Call 504-264-1815. |

| Louisiana Income Tax Credit | Up to $10,000 | Primary residence with homestead exemption | For IBHS-certified FORTIFIED roof installations after July 1, 2025. Subject to $10M annual cap. |

| Construction Code Retrofitting Deduction | 50% of cost, up to $10,000 | Primary residence (not rental) | Deduction on Louisiana income taxes. Effective for taxable periods beginning Jan 1, 2026. |

| Insurance Premium Discount | 22% avg savings | All eligible homeowners with IBHS certificate | Applied to wind/hail portion of premium. Required by law under Act 533 (2024). |

The Louisiana Fortify Homes Program — How the Grant Works

The Louisiana Fortify Homes Program (LFHP) is the state’s flagship grant program, offering up to $10,000 to eligible homeowners to upgrade to a FORTIFIED roof. Here is how the process works:

- Confirm eligibility — Your home must be your primary residence and you must claim the Louisiana homestead exemption on the property.

- Watch for application windows — The LFHP grant lottery opens periodically throughout the year. Spots fill quickly — sometimes within hours. Set a reminder and have your documents ready before the window opens.

- Apply — You will need your homestead exemption tax bill, driver’s license, homeowners insurance declarations page, and flood policy (if applicable). Upload everything at the time of application.

- Lottery selection — If selected, schedule your on-site inspection with a FORTIFIED evaluator within 15 days.

- Choose a FORTIFIED contractor — Only contractors on the Louisiana Fortify Homes roster can access grant funds directly. Get at least three bids and confirm the lead installer holds a current FORTIFIED Roofer credential.

- Complete the installation — The IBHS evaluator returns to certify the completed work meets FORTIFIED standards.

- Receive your IBHS certificate — Upload it to your portal, provide it to your insurance agent, and request the discount at your next renewal.

- Apply for the state income tax credit — For installations completed after July 1, 2025, you may be eligible for a nonrefundable tax credit of up to $10,000. Subject to a $10M annual statewide cap on a first-come, first-served basis.

| Important Grant Timing Note As of late 2025, Louisiana has reached a milestone of over 10,000 FORTIFIED roofs installed statewide, with over 4,000 supported by the Louisiana Fortify Homes Program. An additional 1,300 awards were pending as of December 2025. The program has ongoing state funding — $5 million annually from surplus lines taxes and additional budget appropriations — so new grant rounds are expected to continue. Contact your agent or visit the Louisiana Department of Insurance website to monitor upcoming application windows. Even if a grant window is not currently open, you can begin the FORTIFIED upgrade process now and apply for reimbursement or the next available window when it opens. |

Is Your Home a Good Candidate for a FORTIFIED Roof?

Not every home in Southeast Louisiana will have the same return on investment for a FORTIFIED upgrade — but many will. Here are the factors that make a home a particularly strong candidate:

- Your current roof is aging or approaching replacement age — If you need a new roof anyway, the incremental cost to upgrade to FORTIFIED standards is significantly lower than doing a FORTIFIED retrofit on an otherwise new roof.

- You are in a coastal or near-coastal parish — Homes in Orleans, Jefferson, St. Tammany, St. Charles, Plaquemines, and surrounding parishes face the highest wind risk and typically see the most dramatic premium reductions from FORTIFIED certification.

- Your premium is high — If you are paying significantly above-average premiums, the percentage savings from FORTIFIED are applied to a larger base, meaning your dollar savings are greater.

- Your carrier is admitted in Louisiana — All admitted Louisiana insurers are now required by law to offer FORTIFIED discounts. If your carrier is a surplus lines or non-admitted market, confirm whether the discount applies before committing to the upgrade.

- You are buying a home — If you are purchasing a home, a seller who has already completed a FORTIFIED upgrade is offering you built-in savings from day one. Ask your agent about the IBHS certification status of any home you are considering.

What to Do After You Get Your FORTIFIED Certificate

Getting the IBHS FORTIFIED Roof certificate is only half the job. The other half is making sure your insurance policy reflects the discount you are entitled to. Here is what to do:

- Contact your insurance agent immediately after receiving your IBHS certificate. The certificate is the only document required — per Louisiana Department of Insurance Bulletin 2025-03, no additional hurricane loss mitigation forms should be required.

- Request a premium recalculation at your next renewal — or ask whether you can receive a pro-rated discount mid-term.

- Ask specifically where the discount is being applied — most insurers apply it to the wind and hail portion of your premium. Ask for a premium calculation worksheet showing how the credit is applied.

- If your insurer does not apply the discount or you believe it is being applied incorrectly, contact the Louisiana Department of Insurance at 1-800-259-5300 or visit ldi.la.gov.

- Keep a copy of your certificate in a safe place — digital and physical. You may need it at renewal, when you sell the home, or if you switch carriers.

Louisiana Is Leading the Nation — and It Is Making a Difference

Louisiana is the fastest-growing FORTIFIED market in the country. What started with fewer than 320 IBHS-certified roofs in 2023 has grown to over 10,000 completed installations statewide, with the Greater New Orleans region accounting for a significant share — over 4,000 installations supported by the state program alone.

The top three parishes in terms of total FORTIFIED activity are Jefferson, Orleans, and St. Tammany — the exact communities where Chabert Insurance The Ehrhardt Agency serves clients every day. This is not a distant program or a theoretical discount. It is happening in your neighborhood, and your neighbors are already benefiting from it.

The state’s investment is substantial — $30 million appropriated in 2023, $20 million more in 2024, $15 million in 2025, and now a permanent annual funding stream established through Act 79. Louisiana has committed to making FORTIFIED roofs a cornerstone of its long-term insurance market reform strategy. And under the proposed Regulation 136, the Department of Insurance is moving to standardize and potentially enlarge FORTIFIED discounts even further — making the program even more financially compelling for homeowners who act sooner rather than later.

| A Note from Chabert Insurance We know Louisiana’s insurance market is expensive and complicated — and we know that real solutions are hard to find. The FORTIFIED Roof program is one of the few genuine win-win opportunities available to Louisiana homeowners right now. If you are curious whether a FORTIFIED upgrade makes sense for your home, call us. We can walk you through your current policy, help you understand how much your premium could decrease, and make sure you get every dollar of credit you are entitled to once you complete the upgrade. This is exactly the kind of guidance we are here to provide. |

| Want to Know If a FORTIFIED Roof Could Lower Your Premium? Chabert Insurance The Ehrhardt Agency serves homeowners across New Orleans, Metairie, Mandeville, Covington, and all of Southeast Louisiana. Call us today — we will review your current policy and help you understand exactly what a FORTIFIED Roof could save you. 📞 Call or Text: 504-326-6526 🌐 Visit: protectedbychabert.com 📍 Mandeville & New Orleans, Louisiana |